With the BRICS summit now done and dusted, many people are wondering how the new dynamic will affect South Africa’s economy as well as the direction of international trade and collaboration.

However, when it comes to discussions around BRICS debates are generally quite heated and entirely polarised. Rand Rescue takes a look at some of the latest developments and explores public sentiments around the matter.

Us vs. Them: the problem with polarity

The world has come a long way in the past few centuries, and yet despite all the novel developments and information at the touch of a button we still manage to group most any events or affairs into two extreme poles. Despite logic telling us that things needn’t always be polarised or mutually exclusive - our knee-jerk reaction is to resort to just that.

In South African rhetoric you’d be hard-pressed to find any debate that doesn’t group matters into pre- and post-apartheid, black and white, pro- or anti-BBBEE, and so forth. This phenomenon is quite universal - whether republican vs. democrat, conservative vs. liberal, capitalist vs. socialist, Christian vs. Muslim, rich vs. poor, pro- or anti-vax - it’s hard to find opinions that can accommodate criticism or praise for either of the two options we believe to exist.

That’s not to say that there aren’t circumstances where one absolutely should take a distinct stance, nor that one may not criticise a faction whose antics are detrimental to society - but we’d be remiss to align ourselves so instinctively to any particular side.

In political science, Duverger’s law states that in a contest of two parties all the winnings should be granted to the party who wins the most votes - such as what we see in the US with its two-party system. This law emerged from a hypothesis formed by French political scientist Maurice Duverger who found that a simple majority vote eliminates multi-partism and diversity in politics. This law seems to be set in motion and transpires quite naturally as individuals tend to vote increasingly against opposition as opposed to choosing representatives and parties who truly personify their personal ideals, morals, and aspirations. This tendency is spurred on by the lesser of two evils principle whereby people make choices aimed at mitigating perceived negative impact. The more society gravitates towards such decision-making, the more polarised such society becomes and the less likely it is to introduce other alternatives since these are unlikely to garner sufficient ground-roots support and make any significant impact required to safeguard us from an antithetical force or rule.

It’s no surprise then that most people consider BRICS to either be a force for good or a force for evil and perceive the bloc’s very existence as either a threat or opportunity. This is, of course, a fallacious view. Much of it has to do with the incessant West vs. East fisticuffs - people are of the view that South Africa’s position in the bloc infers undeniable support for evildoers. It’s how these stories are sold to us, after all, but the important point we miss in seeing BRICS nations as wholly corrupt and morally reprehensible is that we forget to examine those nations who oppose them under the same microscope.

Invading other nations is absolutely deplorable, stealing funds from government coffers should never be acceptable, nepotism and cronyism should not be allowed, religious or racial persecution should be eradicated and those in power should answer for their crimes. And yet there’s hardly a nation on earth who abides by these common notions of fairness and justice. Monarchies still exist and make their living off the toil and efforts of the poor - passing on powers based purely on familial association and lineage. Nations like the US have constructed laws that prohibit their persecution in international criminal courts, much like the British crown.

South African leaders like Jacob Zuma, Allan Boesak, Schabir Shaik, Tony Yengeni, Ace Magashule, PW Botha, and Patrica De Lille are among several politicians guilty of misconduct. Likewise, across the globe the likes of John Kirk, Bill Clinton, Adem Smyurek, Eva Kaili, Mick Young, Pier Antonio Panzeri, Tony Abbott, Viktor Yanukovych, Boris Johnson, Andrea Cozzolino, John Stonehouse, Donald Trump, Terrence Cole, Alberto Fujimori, Graham Capill, John Magufuli, John Banks, Yoweri Museveni, Scott Morrison, George W Bush, Robert Mugabe, Richard Nixon, Ricardo Martinelli, Neil Parish, Salman bin Abdulaziz bin Abdulrahman Al Saud, Tony Blair, Mauricio Macri, Daniel Andrews are among thousands of politicians who have been found guilty of misconduct to some extent.

Bearing this in mind, let’s take a look at the BRICS and what the latest developments may mean for our own economy and international relations.

BRICS summit 2023

Heading into the summit, it was already clear that the bloc would make a few pivotal announcements that could shake the political tapestry of the world. While the summit is done and dusted, the impact of these decisions is not yet clear though we can make some assumptions based on global sentiments and economic analyses.

BRICS announced their new members

The BRICS announced during the summit that they will add 6 additional nations to the bloc. In addition to Brazil, Russia, India, China, and South Africa, the BRICS+ group will welcome the following nations officially from 1 January 2024, including:

- Saudi Arabia

- Egypt

- Argentina

- Iran

- Ethiopia

- United Arab Emirates

While the inclusion of some of the new teammates was foreseen, there were certainly some surprises. With nearly 40 autonomous regions having shown interest in joining the bloc, lack of interest was surely not at play - and yet the official tally for BRICS+ 2024 defied many predictions

Unexpected defiance of Putin

The Global North and South Africans alike have lambasted South Africa and other BRICS nations for not taking a hard stance against their Russian partner - and yet the summit proved both Western nations as well as the Putin leadership wrong by choosing to smite both parties. Attendees neither appeased Russian power nor pandered to Western bullying. The rather underwhelming conclusion of the conglomerate was that they don’t condone the war nor owe any other nations fealty for their decisions. It’s perhaps not the hard stance either side wanted, but it’s

BRICS+ resources and trading currencies

The World Mining Data Report 2023 indicates that the BRICS+ group will hold nearly 55% share of the world’s total mineral production once the new members join in January 2024 - this means that all the world’s resources are held between 11 nations. The only data this report excluded was diamonds - since accurate worldwide data for this commodity is not available - the data that is available indicates that the BRICS+ group holds more than 60+ of this resource as well.

To quantify this - consider the USD value of BRICS+ nations’ mineral production.

While all trade in mining production doesn’t occur in USD, it would be significant if the BRICS+ nations decided that their share of production at 46.77% in USD value should exclude USD trade altogether. The BRICS noted that they have no intention of wiping dollar trade off the books as yet, but we need to consider what would happen should they decide to do so.

People tend to conflate trading in a currency for the value of any particular currency - making the assumption that BRICS+ will not be able to unthrone the USD. But the fact of the matter is that the bloc has never made any claims around their intent to replace the dollar. Even if this is not their aim, BRICS+ does not need to enact any drastic measures against the USD to devalue it, they can simply do what they’ve intended to do from the start: no longer sell or buy goods in dollars.

In the lead-up to the summit, many were wondering how the group would position their ‘currency’ to the world. ‘Currency’ is a bit of a misnomer though as the bloc has no intention - at least at present - to create a new central currency. Instead, they’ve launched the Interbank Cooperation Mechanism under the New Development Bank which facilitates digital cross-country local currency payments between participating nations. While the ICM has been operational since 2010, it has not been used extensively by all nations to date.

For the US the problem will also be far more difficult to balance. As the backup currency for trade, they’ve been buffered from inflation in ways not available to other nations. If other places use your currency like gold, then you can mine for your currency almost indefinitely. But if other nations ditch USD trade for other currencies it becomes far more difficult to maintain your deficit and keep inflation in check. This proved pretty futile for Mugabe when he kept printing Zim Dollars - but no one cared for his currency.

And what of other commodities?

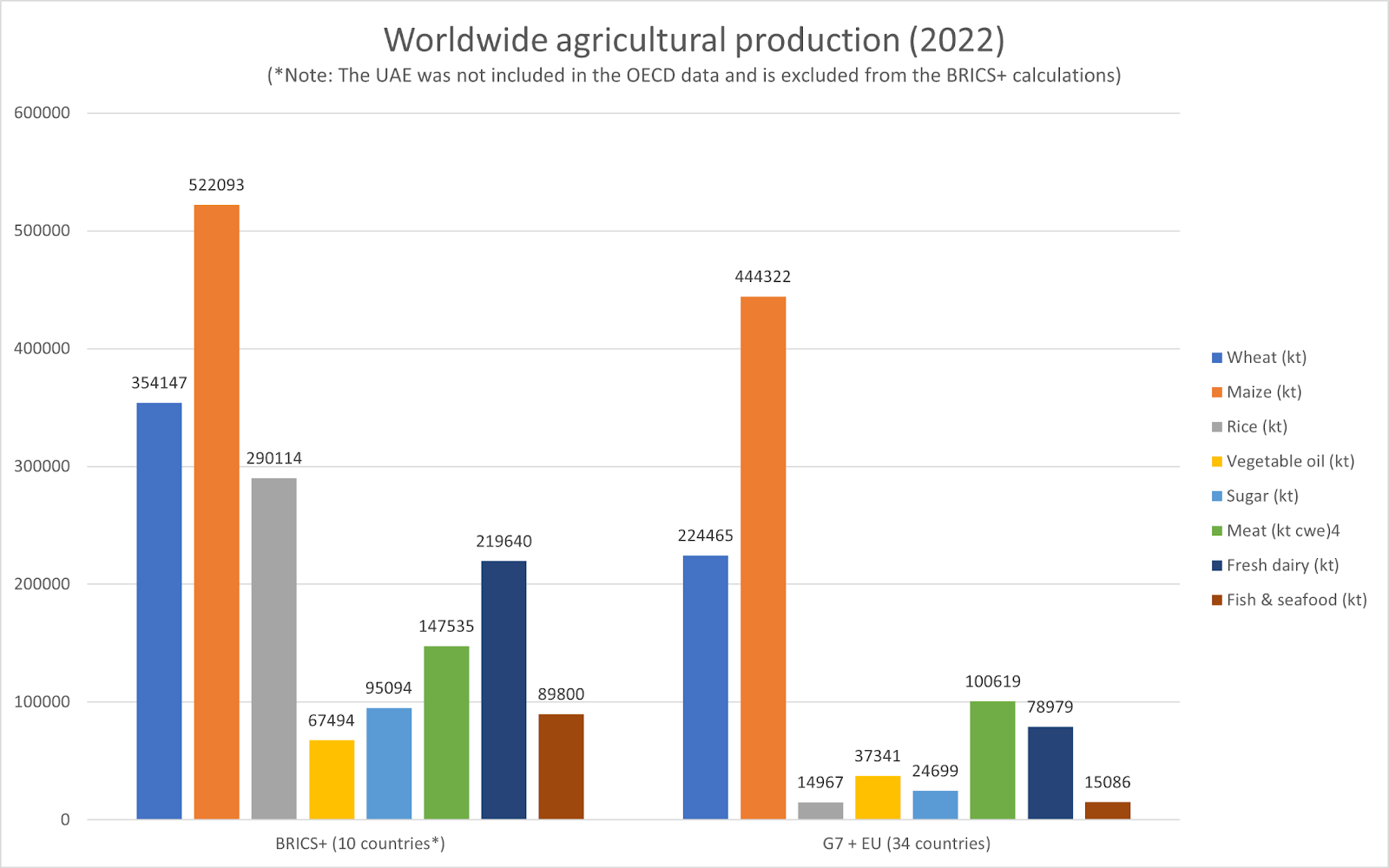

The OECD-FAO Agricultural Outlook report for 2023 - 2032 paints a vivid picture.

The report excluded the UAE from data so we’ve presented the comparison by using 10 of the BRICS+ countries only. Comparing the main agricultural products (wheat, maize, rice, vegetable oil, sugar, meat, fresh dairy, fish & seafood), the 10 countries in the BRICS bloc produce more than the 34 countries in the combined G7 + EU pool.

In contrast, the BRICS+ group consumes more per capita in three of the compared agricultural products, namely wheat, maize, and rice. For all other products compared, the G7 + EU group consumes far more, including vegetable oil, sugar, meat, fresh dairy, fish & seafood as well as cheese. Remember that these numbers are per capita and not per nation.

It’s important to note that the OECD’s report was compiled before 2023 and its estimations still place the USA in pole position for maize production and trade. By their estimates, the US share of global maize production stands at nearly 31% with projections of a slight decrease by 2032 to nearly 30%. But this was before China decided to make drastic changes to their trade agreements and realign themselves with their bloc partners.

This same report places Brazil at a mere 9% of global production at the end of 2022, and yet current estimates - according to Bloomberg now indicate that these two nations’ share of global maize trade will see the U.S. slide to 23% in 2023 and Brazil take a giant leap to 32% of global production. This is the first time since 2013 that the U.S. has lost their no.1 spot. And it will be nearly impossible for the country to regain its position given that the nation who took over their spot sells their yields at 75c per bushel lower than the U.S. It would therefore not just be a matter of renegotiating trade with international partners, but also offering them better deals - something which may cripple the local agricultural market in the U.S. This is good news for South African farmers who also got a massive cut of the U.S. corn trade to China but will undeniably increase tensions between ourselves and foreign trade partners.

The U.S. has buffered export losses in the past by funneling corn supplies towards ethanol plants which is a crucial additive to gasoline production. In fact, around 40% of domestic U.S. crops are currently used for this purpose. But there’s a catch: with the rise in electric vehicle supply and demand the demand for gasoline is also diminishing greatly. The U.S. is not the only player affected by these matters - it’s merely the highest tree in the G7 and other global trade partnerships and drastic changes in trade relations can have a far more sizeable impact on them comparably.

Consider, for instance, BRICS+ and the G7 in terms of global mineral fuel production. Given how reliant nations like the U.S. are on petrodollar recycling there will be several knock-on effects to follow should the global north not manage to negotiate new trade deals with the global south and BRICS+ bloc.

Don’t forget landmass, population and other resources

Between the 11 countries in the BRICS+, the bloc will hold 31% of the world’s total landmass. This is significant for numerous reasons including:

- Arable or recoverable arable land distribution

- Access to natural resources

- Opportunities for relocation or restructuring of civilian zones

- Proportion of coastline distribution

- Variable climatic zones

- Genetic and cultural diversity and skills contribution

- Retention of historical and cultural knowledge and artifacts

- Share of natural organisms and species

- Share of travel and tourism activities

While the BRICS+ group has a far higher rate of population growth comparatively, their share of natural resource use and environmental impact is far less comparatively as well. As with false representation of national production, one also needs to consider the global environmental and climatic impact - and consider all numbers. We’ll cover this in more detail in an upcoming article.

Is trading in USD a prerequisite?

Technically speaking there’s no global stipulation that requires that countries trade in USD or use it as a backup currency - but not doing so could restrict trade with nations who abide by this system of international exchange.

The dollar dominance was the brainchild of former U.S. president Richard Nixon which sprouted from the U.S. Economic Stabilization Act of 1970. This legislation authorised the U.S. president to impose measures to stabilise prices, rents, wages, salaries, dividends and institute price and exchange controls to better protect the U.S. economy. Dubbed the ‘Nixon shock’, it essentially abolished the existing Bretton Woods system used up until 1971. The Bretton Woods system which was instituted in 1944 as an answer to post war debt and international trade. Where currencies were backed by gold before, this system allowed USD conversion to gold at a fixed exchange rate of $35 per ounce. This already favoured the United States since the country could back all gold abroad with dollars and other countries subsequently pegged their own currencies to the dollar.

Due to rising inflation Nixon instituted a series of policy and regulatory changes including wage and price freezes, import surcharges and most significantly a unilateral cancellation of direct international convertibility of the USD to gold. While this cancellation didn’t eliminate the Bretton Woods system directly, foreign nations had no choice but to choose an alternative which eventually saw more and more nations opting for USD stores and trading in this currency. As an additional upshot for the U.S. this meant they could borrow USD abroad at a far lower rate and manage their deficit far easier than other countries.

The dollar is not the only currency held as reserves, although it is most certainly the most dominant.

According to the IMF, the world’s currency reserves for Q1 of 2023 were distributed as follows:

Note, however, that there’s already been a change in this distribution year on year from 2022 to 2023.

While the increase in foreign exchange reserves for ‘Other currencies’ does not seem that sizeable, it’s noteworthy that this group is the only one which has seen an upward trend or increase among all foreign exchange reserves in the past year.

Analysts note in particular that three major ‘reserves’ are to be watched after the BRICS+ bloc is fully operational - including China and the UAE. Of particular importance for South Africans is one of the primary goals noted by BRICS NDB vice president and COO, Vladimir Kazbekov, that the BRICS will invest significantly in the Lesotho Highlands Water Project and that no amount of this trade will be made in USD. Moreover - no parts or resource acquisitions for investment in this project (as well as numerous other infrastructure investments in South Africa) will be made in USD - it will rely solely on exchange between ZAR and whichever of the original BRICS members are party to these agreements and investments.

It’s likely that the BRICS+ will expand the currencies that accommodate such trade to their own affiliates who already trade in their own currencies. For instance - as part of the Common Monetary Area - any BRICS+ investments or trades which are made with the ZAR can also be offered to Namibia, Lesotho and Swaziland who form part of the CMA zone.

Brics+ and the world’s trading routes

Many people seem quite befuddled about Ethiopia's inclusion in the BRICS+ bloc. Among the 11 nations it’s the only one which holds no significant mineral, agricultural, product or exportable service benefits and yet its inclusion speaks to the bloc’s strategic objectives.

Trade routes are of significant geopolitical value for various reasons. One can look back as far as Jan van Riebeeck and his ilk’s antics along the coast of Africa to understand the logistical and economic value of annexing spots along popular trade and travel routes. But perhaps it’s best to consider more recent events.

The impact of political tensions on trade was made patently clear when Russia snubbed Ukraine’s efforts to export grain by preventing Ukrain’s ships from passing through a Russian blockade in the Black Sea. This act of strongarming follows on a slew of acts of Russian aggression in the past years and once more drew ire from numerous fronts - and yet Russia has seesawed on this obstinance since their invasion of Ukraine by allowing the thoroughfare of agricultural products intermittently throughout the conflict. Oddly enough, the blockade has the greatest impact on one of Russia’s closest allies - China - as the major importer of grains from Ukraine. Nevertheless, Beijing has not shown any significant contempt for Russia’s bottlenecking of exports and imports.

These tenuous alliances and hard opposition between nations have unexpected consequences with repercussions that knock-on in unforeseen ways over time. While Ukraine has been highly critical of any nations either not showing support for their country or not taking a hard anti-Russian stance, they also need to maintain a measure of diplomacy in their critique - especially with a nation like China who accounts for 24% of Ukraine’s annual grain exports alone.

It’s becoming increasingly tricky to crunch the numbers cited by various research bodies and media houses as very few of them account for these intricacies. Where the European Commission is quick to cite Ukraine’s contribution to the world’s grain markets they often forget such pivotal points and omit details around the recipients of such exports such as that developed nations account for merely 15,78% of all global wheat imports.

Such data is significant when heeding warnings by the Food and Agriculture Organization (FAO) around global food security. But the answers aren’t as straight-forward and we’d be foolish to assume that an end to Russian aggression would somehow magically restore the global balance of power when developing nations face such challenges irrespective of wars waged further afield.

For nations like the U.K. who renewed their interest in trade with Japan and Australia (among others), trade routes over sea are also of vital importance if one purely considers the geographical proximity of these nations.

The Horn of Africa

Once the new BRICS kids join the bloc the Red Sea and Arabian Gulf will be flanked almost entirely by BRICS+, and although Djibouti, Eritrea and Somalia buffer Ethiopia to the east, one should note that these nations don’t wield the political or economic power to withstand long-term pressures from their neighbours.

The BRICS+ group will also have more discerned group clout along the trade route from Iran past Saudi Arabia and the United Arab Emirates.

Somalia is in a precarious position. Given its weak economy and instability the country has had no choice but to foster alliances with Ethiopia, the UAE as well as the West in order to benefit from investments and humanitarian aid. If renewed clashes in Somaliland are anything to go by, it would seem that factions on either side of the civil divide are stoking fires which will certainly give external parties opportunity to swoop in to seize power or act as bodyguards. The sad reality is that Somali unrest plays into the hands of most any nation seeking to establish a military presence or alternatively feign benevolence through humanitarian aid. This is not to say that all military or humanitarian intervention is questionable - but statistically speaking these external peacekeeping efforts don’t show any significant civilian or socioeconomic benefit over time.

One needn’t don a tinfoil hat to grasp the significance of establishing a permanent foreign presence in the Gulf of Aden.

The United States Institute for Peace has kept a close eye on the region for quite some time - noting that it holds a number of core interests for the US. But the institute had previously assumed that Egypt, Sudan and Ethiopia would maintain their competition over control of the region - presumably not considering that Egypt and Ethiopia would collaborate their efforts as new players in the BRICS+ alliance. The organisation subsequently launched the Red Sea initiative aimed at:

- Bridging the gap in analysing interconnected trans-regional dynamics between the Middle East and Horn of Africa,

- Leveraging their convening authority to work with policymakers in the US, Europe and Asia to overcome institutional divides that impede strategy for a region that traverses traditional geographic divides within bureaucracies and ident, and

- Explore opportunities for new multilateral formats to prevent, mitigate and resolve conflict in the Red Sea region.

U.S. strategy for Africa and the Red Sea arena

Although BRICS has taken tentative power of the Red Sea arena and Horn of Africa, it’s important to consider the strategies and recommendations presented to the US government and already underway to an extent. These goals are outlined in the Red Sea Initiative, U.S. Global Fragility Act 2019 and 2020 National Defense Strategy (among many other acts and strategies):

- Undertaking a sustained diplomatic campaign to broker peace between rival nations in the Horn of Africa and the Middle Eastern blocs and ‘remove the region as battleground for their competition’. One can only guess as to what is inferred by removal of the region as a battleground for competition.

- Catalyse a new regional architecture that minimises contest and maximises cooperation.

- Designate a special envoy for the Red Sea arena OR a deputy secretary of state as interagency lead for developing and executing an integrated strategy for the arena. This would include an interagency policy committee co-chaired by the National Security Council senior directors for Africa and the Middle East.

- Designating the Horn of Africa as a priority under the US Global Fragility Act (2019). This Act authorises initiatives to stabilise conflict-affected areas to prevent violence globally and earmark funding as well as resources by the Department of Defense to protect at-risk areas from terrorist factions.

- Challenge the People’s Republic of China as well as Russian influence in Africa since these countries oppose the Western rules-based international order and advance their own commercial and political interests which weaken U.S. relations with African nations.

- Engage more with African nations given the continent has the fastest-growing population, the second-largest rainforest on earth, 30% of the world’s critical minerals.

- Increase US focus on rule of law in Africa and assist countries to leverage their natural resources, energy resources, critical minerals and supply chains.

- Offer choices to Africans to determine their own future and limit openings for negative state and non-state actions.

- Stem authoritarianism in Africa through a targeted mix of positive inducements and punitive measures such as sanctions.

- Empowering marginalised groups in Africa such as LGBTQI+ individuals, women and youths.

- Invest in locally-led prevention and peace-keeping efforts as well as advance regional stability and security and actors that can provide internal security.

- Prioritise counterterrorism resources to reduce threats to the U.S. Homeland, persons, diplomatic and military facilities including employing tailored programs to build capacity with local partners’ security, intelligence, judicial institutions and networks.

- Leverage and streamline financing and co-investment in local diversified supply chains and advance U.S. and African national security to close the global infrastructure gap.

- Use U.S. influence to develop assistance and financing to help Africa adapt to climate change.

- Pursue public-private partnerships to sustainably develop and secure the critical minerals that will supply clean energy technologies needed to facilitate global energy transition. Including encouraging countries to enact reforms to enable investment in the region’s critical minerals sector.

- Develop a deeper bench of partners by increasing interactions and deploying higher level U.S. interlocutors to promote greater policy alignment based on shared values at multinational forums and international courts.

- Facilitate and support new geographical groupings, deepen U.S. engagement with multilateral institutions and expand foreign partnerships to advance shared goals.

- Utilise the Department of Defense to engage with African partners and highlight risks of Chinese and Russian activities in line with the 2022 National Defense Strategy. Including engaging the U.S. defence private sector in Africa via Prosper Africa to support technologies and energy solutions for African militaries.

- Focus trade and commercial relationship efforts on sectors that align with U.S. policies and increase the use of U.S. Government trade transit cargo security measures.

Hubris, blindsiding or the rise of a New World Order?

It would seem that these initiatives are a case of too-little-too-late in a sense - though the reasons behind this are rather multifaceted. There’s much pandering to the idea of a New World Order nowadays and this concept has many acting out of fear. What we should bear in mind is that such talk is hardly new as shifts in global political alliances, power and structures have occurred throughout the ages.

Such fears emerged during the Dark Ages, Middle Ages, Renaissance, during the Black Plague, at the height of colonialism, when the U.S. fought internally to establish its independence, as Hitler wreaked havoc with his rise to power, with the emergence of the internet, the use of atomic energy, Covid-19, Russia’s invasion of Ukraine. From Napoleon to Obama, Rhodes to Mao, Genghis Khan or Cyril Radcliff, Idi Amin or King Leopoldt III - drastic and devastating shifts in power have littered the landscapes of each continent throughout the ages. Whether a Berlin Wall, Apartheid segregation, Crusades, Samar march, Khmer Rouge, Gulag or Laogai system, or the Troubles - from Wounded Knee to Spioenkop, Torres Strait to the paddies of Vietnam, on the Burma Railway or the chambers of Unit 731 - we’ve seen devastation and major regime change at each turn of human history. In fact, Homo sapiens are widely believed to have gained our position as apex predator and sole human representative walking this earth through deliberate elimination of other hominids, whether through violent elimination or eugenics.

It’s therefore quite crucial not to conflate changing world political systems with any prophetic outcomes - if only for the simple fact that such fear mongering is not a unique phenomenon of the current era of human history. Also consider that different cultures, religions and societies tend to have similar prophecies who all view the ‘other parties’ as evildoers.

The emergence of BRICS does, however, require that we consider how things are changing in the global socio-political and economic landscape. Our yield to polarity makes us vulnerable to hubris and can lead to blindsiding if we deliberately seek out confirmation bias.

The BRICS summit has upended one pivotal assumption made by USIP in their Report on Peace and Security in the Red Sea Arena published in 2020. The report notes:

“US policy should recognize that the external actors responsible for instability in the Red Sea region are not primarily US rivals—that is, China and Russia—but US partners, namely, Qatar, Saudi Arabia, Turkey, and the UAE. Although Iran’s role in Yemen is of course also destabilizing, its influence has not yet reemerged in the Horn to any significant degree. However, Iran, like Russia, could move to exploit instability in the Horn caused by the rivalries of these other states. The United States should consult closely with its European allies as well as important Asian maritime countries, including India, Japan, and South Korea.”

Why South Africa is significant

What the U.S. reports get right is highlighting Africa’s precarious position in proxy wars between opposing global leaders. While the U.K. and U.S. view China, Russia and the Middle East as the culprits in this regard, the same tactics are employed by Europe and North America.

South Africa’s Achilles heel is our desperation. We tend to forget that we will inevitably be beholden to whichever benefactor boosts our status and economy and that each agreement has a long list of caveats which can be exploited or criticised by each of our trading partners irrespective of their ideological or economic alignments. We are at risk of rebuke or exploitation from any party or bloc and sadly our own leaders have not proven their mirth and steadfast pursuit of South African civilian upliftment which would safeguard us from the corruption which flourishes quite unencumbered amid drastic policy and power shifts.

Why would a sub-par nation have so much clout?

It’s understandable that the underdog who’s always clutched at the short end of the stick would feel like one of the cool kids for once. Who wouldn’t want to be no. 5 of 5 when you’ve hovered in the 100s on various global tallies for so long? Especially if one looks at the numbers and realise that South Africa is placed 11th in the world for all mineral and mining production globally. If it were a sporting event, one would certainly feel more confident when your team in the top 20 comprises 7 players while the opposing team only has 3.

Perhaps we should focus on other numbers - such as the world’s most precious and rare metal - Rhodium - which South Africa holds 80% of total worldwide production and/or perceived stores (the data represented in reports is rather vague and does not clearly delineate between existing production and unmined ores). Not only is it the most valuable ore - but its applications have increased significantly given its usage in manufacturing of automotive, industrial and scientific equipment and materials. Rhodium comprises 80% of catalytic converter material for existing automobiles, but unlike other metals it is not limited to this singular application or industry. One of the primary benefits of using Rhodium as opposed to other platinum minerals is that it does not readily produce nitrogen and oxygen.

Facts about Rhodium:

- Most valuable metal on earth: $15 250/troy/ounce

- SA’s contribution: 80% of global production

- Melting point: 1 964°C

- Retains its lustre

Facts about Iridium:

- Second most valuable metal: $4 750/troy ounce

- SA’s contribution: 87% of global production (with remaining ores found almost exclusively in Zimbabwe, Russia and Canada)

- Melting point of 2 226°C

Facts about Osmium:

- Densest metal on earth

- SA’s contribution: 12,3% of global production (limited global supply)

- Melting point of 3 033°C | Boiling point of 5 008°C

- Share of USD trade - predominantly from Chinese Taipei ($139M)

These are but a few precious metals which are found within South African borders and quite pivotal in the trade agreements we’ve formed in recent years.

It’s not just about finance and resources

While our constitution and legal frameworks are hypothetically quite sound and representative of a free and democratic nation - such frameworks and regulations are merely emblematic if the entities who uphold them lack the power to act on those rules of law stipulated in our legislation. Our legislation has, for instance, been used as a template for structuring laws and human rights frameworks the world over - from India and the USA to New Zealand and Sweden. But as with so many things which have deteriorated in SA’s recent history, our legislators seem to have lost their hold on those mandates which instruct them to operate as unbiased watchdogs and judges who hold our leaders to account.

When one of our trading partners accuses the other of war crimes or human rights atrocities we seem to forget that such claimants are guilty of similar blunders. Iran and Libya have called on the U.S. to answer for war crimes committed on their turf, while the U.S. has called on Russia and China to answer for their own crimes in Ukraine and Taiwan. Europe has lambasted Africa for corruption and mismanagement of financial resources and tools while facing a debt crisis orchestrated by their own ineptitude. The world is quick to point out South Africa’s sordid Apartheid history by plays mum in events that transpire in Israel and Palestine. While the U.S. policies aim to uphold the rights of women and LGBTQI+ groups in Africa - it has backtracked decades in its own support of rights for such groups with drastic draconian legislation which denies reproductive and healthcare to such groups.

We should bear in mind that the stats about resources and trade don’t represent the whole picture - society and culture are massive players in politics.

The decay of our natural resources amid climate change, loss of cultural identity, hogging of stolen artefacts by superpowers, religious and gender identities are all factors at play in the restructuring of the strange new world we live in.

BRICS+ requires better leadership

South Africa’s weakness is quite clearly that we are beholden to our benefactors due to the fragile state of our economy. The question is not whether we - along with other territories who enter the race on the back foot - are being exploited by global powers, but rather which powers will grant us an opportunity to grow our own strengths most significantly to the benefit of our own people.

Given how powerful BRICS+ can become in terms of the global geopolitical and socioeconomic landscape it’s crucial that SA focus on strong leaders and that all of us - whether still rooted and living in the nation or settled abroad - understand our individual roles, opportunities and risks which relevant to the bloc’s expansion.

While we certainly should throw our weight behind those ideologies or factions we support most - we should plan ahead, strategise and consider what would be most beneficial to our own livelihoods as well as the survival and progress of our businesses and life’s work.

We’ll help you navigate cross-border transactions.

If you're planning on moving abroad or already living in a new country, let Rand Rescue assist in your cross-border transactions and advise on the best decisions for your portfolio.

Note: Rand Rescue draws on numerous sources, views and research data for our articles to ensure an objective representation and holistic view of affairs. While our content explores a wide scope of views and data, citation does not infer promotion or accuracy of all views as some sources are prone to confirmation bias or flawed data parsing. Partisan, unconfirmed or inaccurate sources should always be considered within the context of the narrative and may not be quoted in isolation or misrepresent our intent, observations, or conclusions to other readers. Users are urged to link to our original articles wherever possible.